Minimising home country bias.

Home country bias refers to the tendency to favour local investments. The result is decreased diversity, increased risk, and potentially missed profitable opportunities.

One factor that contributes to home country bias is the complexity of foreign currency exchange rates when a portfolio has exposure to multiple currencies. The exchange rates of each currency to every other currency needs to be considered to reduce risk and maximise growth. Converting the portfolio to one currency (the home currency or US dollars or sterling pound) does not use all the exchange rates, and so neglects important information.

CLCI has developed the CLCI Global Benchmark Index (GBI) which is used to convert currency exposures in a portfolio to currency neutral values that can be used to provide non-biased measures of risk and return.

Maximizing global wealth in an absolute sense should be the goal of all rational investors. The indices developed by CLCI seek to do this by redefining the way in which risk is measured and in doing so also determining non arbitrary benchmarks for risk and return. Home country bias has been one of the most persistent anomalies in finance and while information asymmetry, regulatory hurdles and transaction frictions have in the past partly explained this apparent anomaly the internationalization of financial markets in more recent times has made the lack of international perspective of most market participants even more perplexing. This bias leads to a distortion in the perception of risk and return. The CLCI optimization methodology redefines the “riskless asset” as an optimally weighted basket of currencies. CLCI Global Benchmark Index (GBI). Using CLCI-GBI as a common base for all exposures allows risk and return to be managed and understood in the global context.

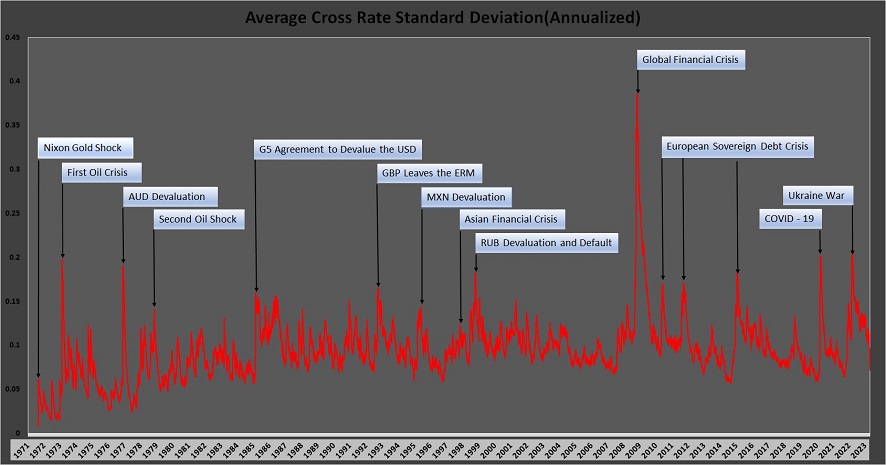

CLCI has developed proprietary valuation metrics for the selected core group of currencies that work in real time to measure deviations from purchasing power parity, as well as trends in capital flows.

The CLCI Global Value Index (GVI) has been calculated back to August 1971 and has displayed significant outperformance over time, while the GVI/GBI return standard deviation over time has been lower than that for any freely floating individual currency in the selected currency group using GBI as the common base.